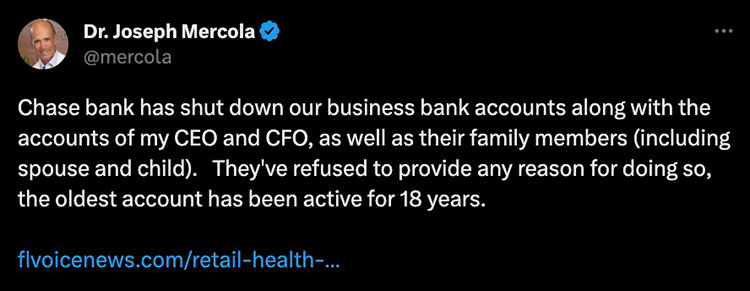

TheEpochTimes.com

Large money-center banks appear to be in the vanguard of a movement to build a system of personal social credit scores.

This week, British bank Barclays became the latest to be accused of shutting the accounts of its customers for political or religious reasons. This followed revelations in April that Coutts, a private bank owned by British Bank NatWest, was alleged to have closed the accounts and publicized personal information of conservative politician Nigel Farage, one of the foremost Brexit advocates and a supporter of the policies of former U.S. President Donald Trump.

And British banks are not alone. Many say that America’s largest banks are in lockstep with UK banks in establishing political and social criteria for their customers, and punishing those who don’t comply.

“Sadly, what we're seeing now with NatWest and Barclays isn't surprising,” Justin Haskins, director at the Heartland Institute, told The Epoch Times. “There is a mountain of evidence that shows many of America's largest and most powerful banks are discriminating against customers because of their ideological, social, cultural, religious, or political views.”

Continue Reading

Rating: 0.00/5 (0 votes cast)